Vietnam’s policy direction has clearly pushed for prudent antibiotic use. But do local veterinary-drug manufacturers already move in lockstep with that intent? Using import statistics for active pharmaceutical ingredients (APIs), we review how Vietnam’s antibiotic-API inflows evolved from 2022 to 2024—and what those shifts reveal about real demand on the ground.

Trends over time

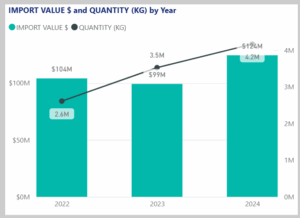

- 2022: imports totaled about $104M and 2.6M kg.

- 2023: value slipped to ~$99M while quantity rose to ~3.5M kg → price easing, tougher procurement, and inventory building rather than a demand collapse.

- 2024: value and volume climbed together (~$124M; ~4.2M kg) → herd recovery, normalized global pricing, and renewed downstream usage.

- Net read: stewardship intent is visible, but the market adjusted via pricing and stock strategies first; underlying consumption recovered in 2024

By active ingredient (value leaders)

- Amoxicillin (~$73M): anchor β-lactam, broad coverage and strong cost-effectiveness.

- Doxycycline (~$53M): versatile tetracycline for respiratory/enteric diseases in swine and poultry.

- Florfenicol (~$32M) and cefotaxime (~$27M): core for respiratory syndromes; used as second-line or combination choices.

- Oxytetracycline (~$16M): legacy workhorse, still relevant in field protocols.

- Tylosin, tiamulin, colistin (each ~12M): targeted use for mycoplasma, dysentery, and severe Gram-negative control; stewardship-sensitive.

- Gentamycin (~$10M), tilmicosin (~$8M), fosfomycin (~$6M), enrofloxacin (~$6M): the long tail that ensures therapeutic optionality.

- Message: manufacturers optimized within familiar classes; no dramatic pivot away from antibiotics is evident in the API mix.

By country of origin:

- China ≈ 94.7% of value (~$310M across 2022–2024): scale, price, and dossier readiness drive dominance.

- India ≈ 4.4% (~$14M): selective alternatives; useful for risk diversification.

- Others ≈ 0.9%: marginal.

- Risk note: heavy single-hub exposure raises vulnerability to price spikes, regulatory shifts, or logistics disruptions.

Implications for companies

- Expect a gradual taper in antibiotic intensity, not an abrupt drop; policy, vaccines, and biosecurity adoption must accelerate to bend the curve faster.

- 2023’s “value-down, volume-up” shows procurement discipline—leverage competitive tendering and forward buys when prices soften.

- Consider dual-sourcing critical APIs (China + India/EU) to hedge supply shocks, even at slightly higher landed costs.

- Watch stewardship-sensitive molecules (e.g., colistin, fluoroquinolones) for potential regulatory tightening and reformulate portfolios proactively.

Conclusion

- Vietnam’s manufacturers remain anchored to affordable, proven antibiotics, with 2024 indicating demand recovery. Change is evolutionary: cost, availability, and field realities still shape buying more than policy alone.

ALAU VIETNAM provides comprehensive market-research reports on veterinary medicines, API imports, feed additives, disinfectants, and vaccines. For detailed datasets or custom analysis, please contact us.